The expensive on-ramp mistake is thinking the checkout provider is the whole bill. It is not. MoonPay, Transak, and Ramp can all get fiat into crypto, but the final cost depends on payment method, spread, network fees, partner markups, bank charges, and whether the quote changes before settlement.

My default pick is Ramp Network if you are buying directly and want the clearest fee table before you start. Ramp publishes method-specific fee caps for direct purchases, and it separates Ramp's fee, network fee, optional partner fee, and bank-side charges in plain sight.

MoonPay is the better fit when the product you are already using has a polished MoonPay-powered checkout, especially after its May 2026 Headless Onramps launch. Transak is the practical fallback when your wallet, dApp, country, or asset support lines up better through Transak. But if the question is "which one lets me inspect the cost model fastest?", Ramp is the cleanest starting point.

I checked official fee disclosures, the current MoonPay Headless Onramps announcement, Ramp and Transak help/docs pages, public evidence screenshots, current SERP competitors, GDT operator data, and concrete public buyer-question patterns. I did not create accounts, submit KYC, link a card, run a bank transfer, accept a quote, receive crypto, test sell/off-ramp flows, or contact support. This is a buying-decision guide, not a live transaction test.

If you are choosing an exchange instead of a wallet-first checkout, start with our crypto exchange guide or the narrower Kraken vs Coinbase comparison. If you already hold coins and only need swaps, our non-custodial exchange roundup is the better next read. And if this is a long-term balance, sort out hardware wallet storage before checkout convenience becomes a custody plan.

-

#1 Ramp NetworkBest direct-fee visibility: explicit fee table, direct wallet delivery, and clear partner-fee caveat

-

#2 MoonPayBest embedded checkout momentum: strong wallet/app partner story and new headless on-ramp flow

-

#3 TransakBest when your wallet or dApp already routes through it and you need asset/country fit more than a fixed fee table

If I were buying straight to a self-custody wallet today, I would start by checking Ramp Network . If the wallet I was already inside offered a native-looking MoonPay route, I would compare the quote instead of reflexively leaving the flow. If the available route was Transak , I would inspect the exchange rate, third-party fees, and quote validity before accepting.

How I ranked these on-ramps

I ranked this as a buyer decision, not as a brand-size contest. The question is not which company has the largest partner list or the nicest checkout. The question is which route gives a normal buyer enough information to decide before money leaves the bank.

Fee clarity came first. A provider that separates provider fee, network fee, partner fee, bank-side risk, and exchange-rate behavior is easier to trust than one that makes the buyer infer everything from the final quote.

The delivered amount wins.

Payment rails came next because the rail often changes the price. Card, bank transfer, Apple Pay, Google Pay, PayPal, and Pix are not interchangeable. A cheap bank route can lose to a card route if the bank transfer is unavailable, slow, or unsupported in your country. A card route can lose badly if issuer fees or foreign-transaction fees show up later.

Wallet delivery was the third filter. The best on-ramp should get the asset to the right wallet on the right chain with the least confusion. A clean provider fee is not useful if the checkout nudges buyers into the wrong network or makes the destination hard to verify.

The route matters.

Partner markup risk was the fourth filter. This is where buyers get caught. Direct provider pages tell one story; embedded wallet, marketplace, or dApp checkout can tell another. Ramp gets credit because its fee page explicitly calls out optional partner fees. MoonPay gets credit because the embedded checkout strategy is real, but the partner context also makes universal fee claims dangerous. Transak gets credit for explaining quote mechanics, but the buyer has to move carefully.

Buyer fit came last because the "best" provider is still conditional. Ramp is my default starting quote. MoonPay can be the better pick inside a trusted app. Transak can be the better pick when your country, asset, chain, or wallet path lines up there first.

Cheapest is not enough.

MoonPay vs Transak vs Ramp comparison table

| Feature | Ramp Network | MoonPay | Transak |

|---|---|---|---|

| Best job | Direct wallet-first purchase with the clearest public fee breakdown | Embedded wallet/app checkout and broad partner distribution | Wallet/dApp route where Transak already has the best local support |

| Fee proof | Publishes method-specific direct fee caps plus network, partner, and bank-fee caveats | Pricing disclosure says fees vary by order, geography, partner, method, spread, and other costs | Help article separates Transak fee, third-party fees, spread, and quote validity |

| Payment rails | Cards, bank transfers, Apple Pay, Google Pay, Pix in supported regions | Cards, Apple Pay, Google Pay, bank transfer, PayPal where supported | On-ramp/off-ramp rails vary by country, fiat currency, payment method, and asset |

| Hidden-cost check | Partner fees can appear in embedded flows; direct Ramp pricing is not always partner pricing | Bank-related fees, spread, network fee, and partner context matter | Exchange rate is short-lived and final price can refresh if you wait too long |

| Delivery shape | Buy crypto directly to your wallet | Hosted or embedded purchase route; Headless Onramps launched May 2026 | Fiat-to-crypto inside partner apps and direct purchase flows |

| Skip if | Your region, asset, or wallet integration routes cheaper through another provider | You need a simple public fee table before entering the checkout | You want the easiest direct public fee table or hate quote-refresh risk |

| Action | Compare Ramp | Compare MoonPay | Compare Transak |

The real on-ramp bill has five moving parts

Crypto on-ramp pages make buying feel like a single button. The cost model is closer to airline checkout. The provider fee is one line. The payment method changes another. The spread or exchange-rate adjustment can be baked into the quoted rate. The network fee moves by chain and congestion. A wallet, marketplace, or dApp partner may add its own markup. Your bank can still add a foreign-transaction, card, or currency-conversion fee.

The trap is that the cleanest checkout can be the least comparable one. A native wallet button feels safer because it is already inside the app. But the route behind that button may bundle provider economics, partner economics, and payment-rail costs in a way that makes a direct quote look different.

That is why "MoonPay is expensive" or "Ramp is cheap" is too blunt to be useful. The right question is: who shows enough of the bill before I authorize payment, and does the route match the job?

The real comparison is delivered crypto under identical route conditions.

Ramp is strongest on that first question because its support page exposes a direct fee structure. MoonPay is strongest when the product experience matters because the company is pushing checkout deeper into partner apps. Transak sits between those worlds: broad integration surface, clear fee-calculation language, but a quote flow where you need to respect timing.

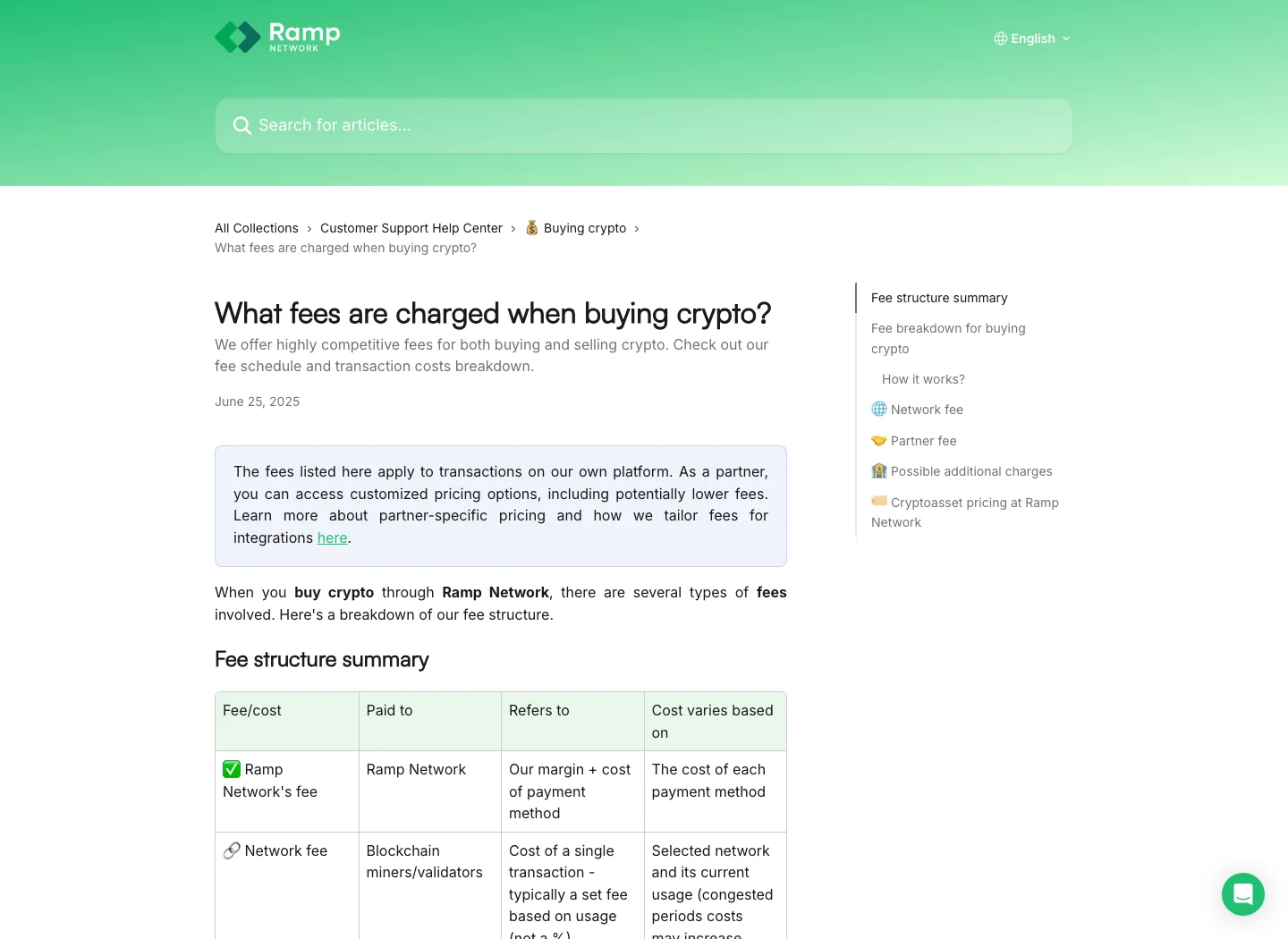

1. Ramp Network: best default when fee visibility matters most

Ramp wins the default slot because its public fee page is the easiest one to reason about before you open a checkout. The page separates Ramp Network's fee, network fee, optional partner fee, and bank-side charges. It also says the direct fees apply to Ramp's own platform, while partners can have customized pricing.

That last caveat is important. If you buy through Ramp directly, you are looking at Ramp's direct setup. If you buy inside a wallet or marketplace that embeds Ramp, the partner may add a fee. That does not make Ramp bad. It makes the exact checkout context matter.

The fee table is still useful. Ramp lists bank transfers, easy bank transfers, cards, Apple Pay, Google Pay, and Pix, with method-specific caps for direct purchases. Cards can cost more than bank transfers. Apple Pay and Google Pay follow the underlying card. Network fees are separate and paid to validators/miners, not Ramp. Bank-side currency fees can still exist outside Ramp's control.

That is the level of disclosure I want from an on-ramp. Not because it guarantees the cheapest quote, but because it gives the buyer a checklist before they click. If a partner checkout hides the partner fee or makes the delivered crypto amount hard to compare, you can back out and run the same amount through direct Ramp, MoonPay, or Transak.

The weakness is coverage and context. Ramp can be the best direct purchase route for one buyer and not available, not cheapest, or not the smoothest for another. Your country, fiat currency, asset, chain, payment method, and wallet destination still decide the final quote.

Ramp publishes the clearest direct fee breakdown here, separating its fee, network fee, optional partner fee, and bank-side charges.

Skip it if your exact country, asset, or wallet route is better supported through MoonPay or Transak, or if an embedded partner route adds a markup you cannot justify.

Ramp ranks first because direct fee visibility and wallet-first delivery make it the safest default starting quote, even though availability and partner pricing can change the answer.

- Clearest public direct fee table among the three providers checked

- Separates provider fee, network fee, optional partner fee, and bank-side charges

- Strong fit for buying directly to a self-custody wallet

- Apple Pay and Google Pay support follow the underlying card logic

- Partner checkout pricing can differ from direct Ramp pricing

- Final quote still depends on region, currency, asset, chain, and payment method

- Network fees and bank-side currency/card charges can sit outside Ramp control

- No live account, KYC, card authorization, delivery, or support test was performed

2. MoonPay: best embedded checkout story

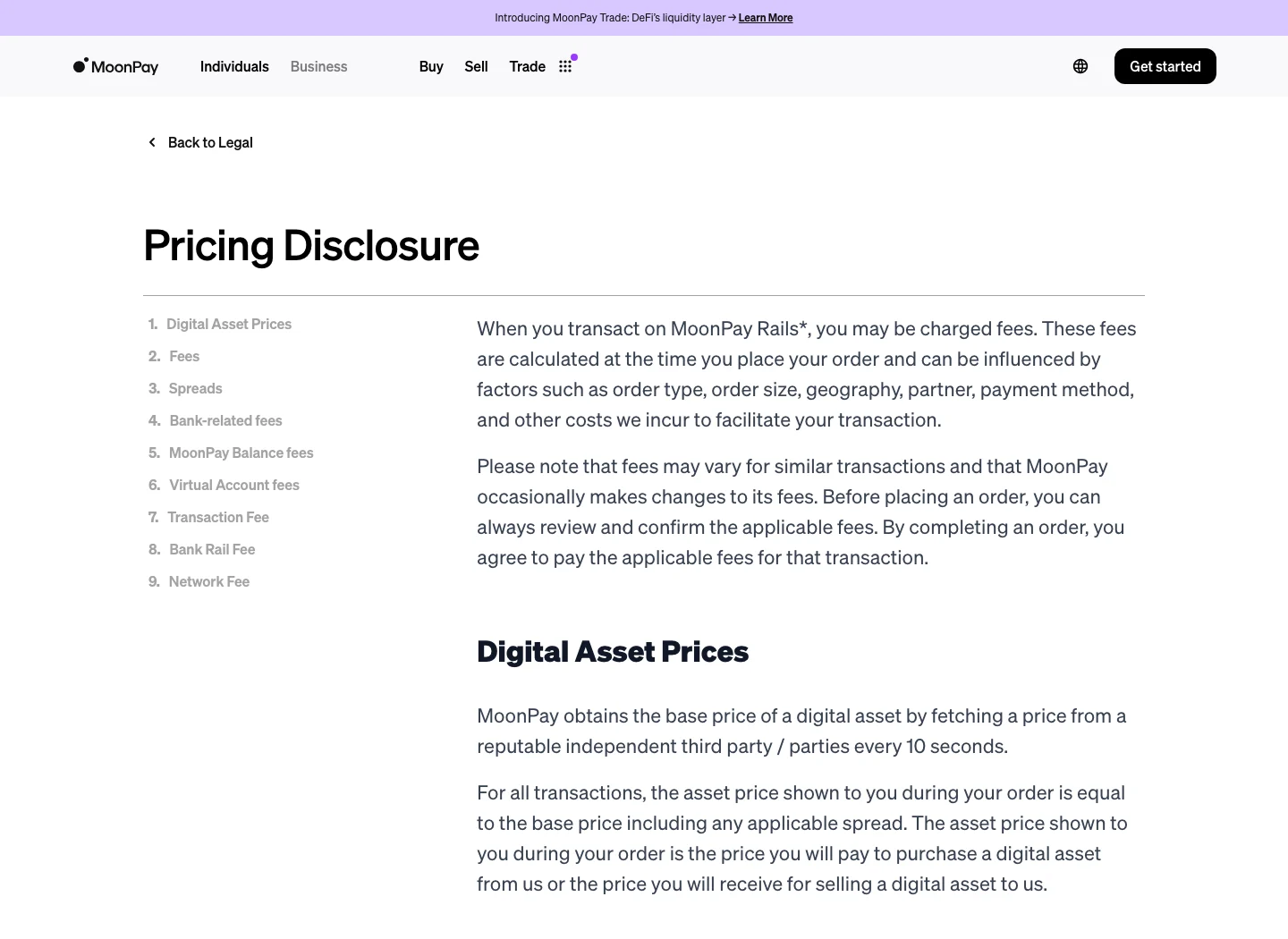

MoonPay is not second because it is weak. It is second because the buyer question here is cost visibility, and MoonPay's public disclosure is more variable by design. The pricing disclosure says MoonPay Rails fees are calculated when you place the order and can be influenced by order type, order size, geography, partner, payment method, and other costs. It also calls out spreads, bank-related fees, transaction fees, bank rail fees, and network fees.

The upside is distribution and checkout experience. MoonPay's May 14, 2026 Headless Onramps launch is a real product-context shift: the company says partners can embed native Apple Pay, card, and Google Pay purchases across the US, EEA, and 100+ countries while MoonPay handles payment rails, compliance, and identity verification underneath.

That matters because many buyers never choose an on-ramp from a blank search page. They are inside a wallet, marketplace, game, exchange-adjacent app, or DeFi product. If that app presents a MoonPay route that is native, fast, and easy to confirm, the winning move might be to compare the delivered crypto amount rather than leave the app to chase a theoretical cheaper provider.

The catch is the same thing that makes MoonPay powerful: partner context. A MoonPay quote inside one app can feel different from a MoonPay route somewhere else. The provider fee, partner economics, selected payment method, and bank/card behavior can all matter. Treat MoonPay as a strong checkout network, not a promise that every MoonPay-powered button is the cheapest button.

MoonPay's Headless Onramps launch makes the embedded partner checkout story stronger, especially for wallet and app flows where leaving the product adds friction.

Skip it if you need a public method-by-method fee table before entering checkout, or if the partner route makes the delivered crypto amount hard to compare.

MoonPay scores high for payment reach and embedded UX, but loses the top slot because the official fee disclosure is variable and partner-dependent rather than table-first.

- Strong wallet, app, and partner checkout distribution

- Headless Onramps launched in May 2026 with Apple Pay, card, and Google Pay support

- Official disclosure says fees are reviewed before placing an order

- Good fit when the product you already use exposes MoonPay cleanly

- Fee disclosure is variable by order, geography, partner, method, spread, and other costs

- Partner context can make one MoonPay checkout different from another

- Bank-related and network fees can sit outside the visible provider fee

- No live quote, purchase, KYC, delivery, or support workflow was tested here

3. Transak: best when route availability is the deciding factor

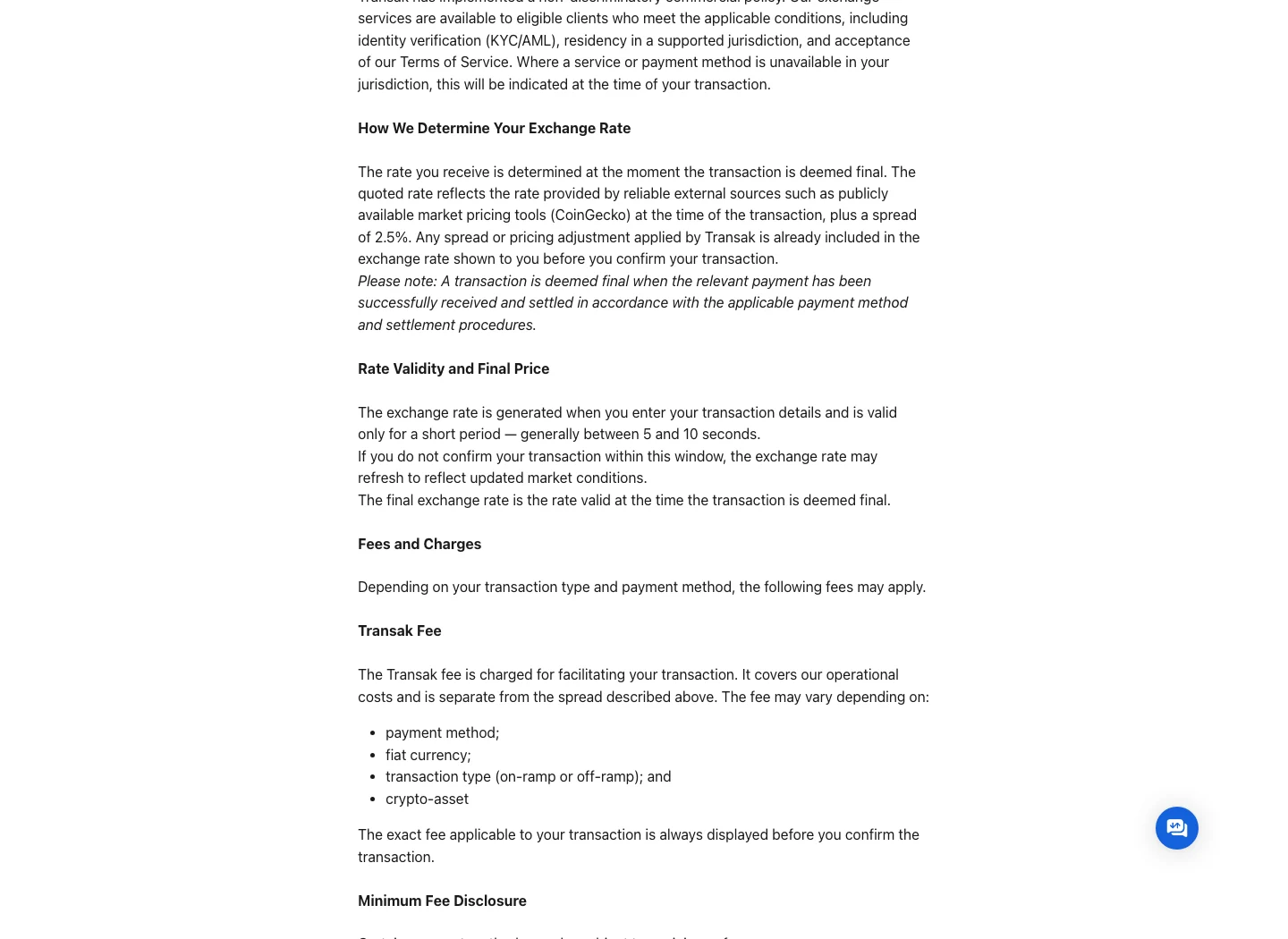

Transak is the one I would not dismiss just because it ranks third. If your wallet, dApp, or country has a better Transak route than the alternatives, the practical answer can be Transak. The docs position it as a fiat on-ramp/off-ramp layer for buying crypto with fiat inside applications, and the help center gives a useful breakdown of how prices and fees are calculated.

The important disclosure is quote mechanics. Transak says the quoted rate reflects pricing from external market sources plus a spread, and any spread or pricing adjustment is included in the exchange rate shown before confirmation. It also says the exchange rate is generally valid for only a short period, typically between 5 and 10 seconds. If you wait too long, the rate can refresh.

That does not make Transak uniquely risky. It makes the checkout timing more explicit. You need to compare the final delivered amount, not just the visible fee label. You also need to check third-party fees, fiat currency, payment method, transaction type, crypto asset, and network-specific delivery details before authorizing.

Where Transak can win is support fit. On-ramp providers are not interchangeable if one supports your asset, chain, local payment method, and wallet path better than the others. A slightly less elegant fee disclosure can be worth it if the alternative is a failed card route, unsupported currency, or asset unavailable in your region.

Transak documents the exchange-rate, spread, third-party fee, and short quote-validity mechanics buyers need to understand before accepting.

Skip it when Ramp or MoonPay gives you a clearer delivered-amount comparison for the same country, asset, chain, and payment method.

Transak ranks third for default buyers because the quote flow requires more attention, but it remains valuable when asset, country, wallet, or dApp support lines up better.

- Useful in wallet and dApp flows where Transak has better local support

- Official help material explains fee variables and quote validity

- Spread or pricing adjustment is included in the shown exchange rate before confirmation

- Strong fit when asset, chain, fiat currency, and payment method coverage decide the purchase

- Short quote-validity window can refresh the exchange rate if you hesitate

- Final cost depends on third-party fees, method, asset, currency, region, and settlement timing

- Less table-first than Ramp for a buyer comparing direct fee caps

- No live payment, KYC approval, wallet delivery, or support flow was tested

How to choose without getting clipped

Run the same amount through all available routes and compare the delivered crypto amount, not the headline fee. Use the same asset, chain, payment method, fiat currency, and wallet destination. If one quote uses card and another uses bank transfer, you are not comparing providers anymore. You are comparing rails.

Then check the partner context. Direct Ramp can be different from Ramp inside a wallet. MoonPay inside a partner app can differ from MoonPay's hosted route. Transak inside a dApp can be the only route that supports your local method. The partner surface is part of the product.

Finally, decide what happens after the buy. If the crypto lands in your own wallet, verify the address, chain, and recovery setup before sending a meaningful amount. If you are buying through an exchange instead, you may want Bitcoin DCA apps, tax software, or seed phrase backup hardware more than another on-ramp comparison.

The quote check I would run before paying

Do this before you authorize anything. Open the same purchase in every route you can access. Use the same fiat amount, same asset, same chain, same destination wallet, and same payment method. If one provider is using debit card and another is using bank transfer, stop. You are not comparing MoonPay vs Transak vs Ramp anymore. You are comparing card rails against bank rails.

The buyer is not trying to admire a payments stack; the buyer is trying to avoid a bad surprise.

The real mistake is trusting the route because the logo is familiar.

This is where many wallet-first buyers overlook the real trap: the provider name is less important than the route.

This is where the buyer has to slow down.

The catch is psychological. A familiar wallet button lowers the user's guard before the quote earns it.

Here is the thing: beginners rarely lose money because they forgot the provider name. They lose it because the chain, rail, partner fee, or bank fee changed.

Many buyers notice the bank fee only on statement day.

Many on-ramp comparisons go sideways right here. They compare provider names when they should compare route conditions.

First, write down the delivered amount. Not the fee label. The delivered amount. If you are spending $250, the useful comparison is how much BTC, ETH, SOL, USDC, or whatever asset reaches the destination after the provider fee, spread, network fee, and partner markup are applied. A provider with a prettier fee label can still deliver less crypto.

Second, open the details drawer before you approve the quote. On a good checkout, you should be able to identify the payment method, provider fee, network fee or chain cost, exchange rate, destination network, and any partner or service fee. If those lines are absent or bundled into one vague total, I would treat that as a reason to compare another route before buying.

The hard part is not finding a buy button. The hard part is knowing what that button bundles.

Third, check whether the quote is direct or embedded. Direct Ramp is one route. Ramp inside a wallet is another route. MoonPay in a partner app is not always the same as MoonPay's hosted flow. Transak inside a dApp can be the best local option even if the public fee language looks less table-friendly. The app around the on-ramp can change the bill.

Fourth, use the smallest first transaction that still makes sense. I do not like sending a meaningful amount through any new on-ramp until I have seen the wallet delivery path, receipt detail, and chain selection behave the way I expect. That is not paranoia. It is just cheaper than learning you bought the wrong asset on the wrong network after the real money moved.

The boring move is to reject any quote you cannot break apart.

Fifth, save the receipt and transaction details. On-ramp buys can create tax records, wallet histories, and proof-of-funds questions later. If this purchase becomes part of a larger stack, your future self will care which route you used, what the delivered amount was, and which wallet received it.

How Reddit question patterns were handled

Reddit was checked because on-ramp pain usually shows up as questions before it shows up in clean documentation. The useful pattern was not "people like or dislike MoonPay." That would be too sloppy. The useful pattern was concrete: r/BitcoinBeginners questions around delivered amount, r/Moonpay questions around bank-side fees, and r/sgcrypto questions around pending or failed Ramp routes.

Reddit is bad evidence for ranking sentiment. A thread can overrepresent angry users, unlucky failures, regional quirks, or scams that used a provider name in the story without proving the provider caused the loss. So Reddit did not become a popularity score, trust score, support score, or failure-rate estimate. It became a checklist for the doubts this article needed to answer: delivered amount, bank charges, quote timing, pending states, and partner context.

That is why the article keeps returning to the same boring test: compare delivered crypto for the same route conditions. If a Reddit question says "I bought through MoonPay and got less than expected," the professional response is not to declare MoonPay good or bad from one thread. It is to ask which payment method, which partner app, which asset, which chain, which bank fee, which network fee, and which quote screen were involved.

The same applies to Ramp and Transak. A pending or failed payment story can be a provider issue, a bank issue, a compliance hold, a chain/network delay, a scam website impersonating a route, or a user sending funds to the wrong destination. Without transaction receipts and support records, you cannot responsibly turn those stories into performance claims. You can, however, turn them into buyer protections: use official URLs, start small, check the destination network, save receipts, and do not confuse a wallet's embedded button with universal provider pricing.

The verdict

Choose Ramp Network first when you want the fastest public fee sanity check and direct wallet delivery. Choose MoonPay when the checkout is already embedded in a product you trust and the delivered amount is competitive. Choose Transak when route availability, country support, asset support, or wallet integration beats the other two.

The best habit is boring: compare the delivered crypto amount, confirm the payment rail, check partner fees, account for your bank, and do a small first transaction before moving real money. The on-ramp is the bridge. It should not become the part of the stack you trust blindly.